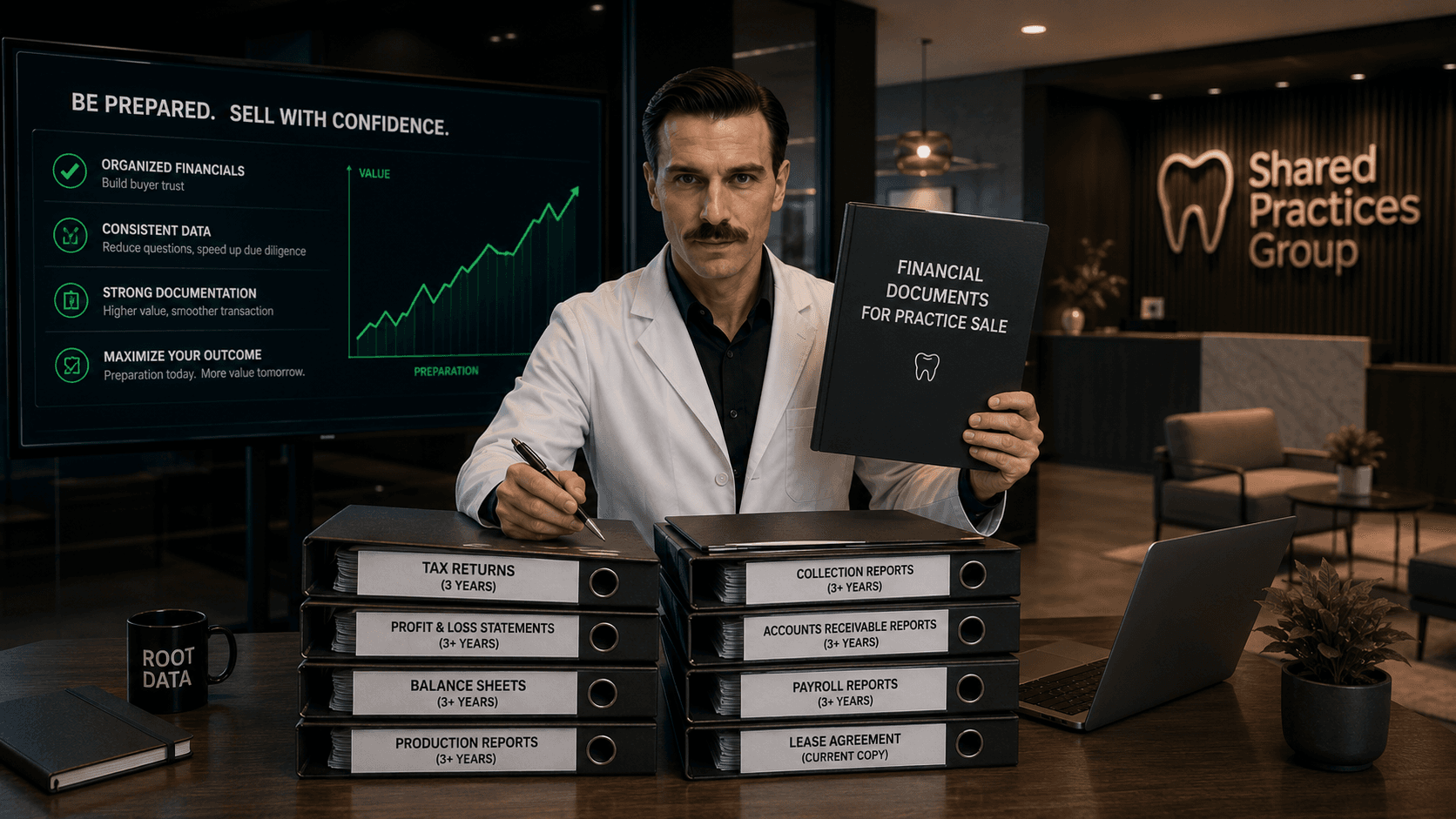

What Financial Documents Do You Need to Sell a Dental Practice?

A dental practice sale often stalls if the seller lacks clear, consistent financial records. Buyers need a transparent view of your business. They want to see where your revenue comes from, how you manage expenses, and if the profits will remain stable after you leave. When your reports are scattered or your numbers conflict, buyers lose confidence and pull back.

A dental practice sale often stalls if the seller lacks clear, consistent financial records.

Buyers need a transparent view of your business. They want to see where your revenue comes from, how you manage expenses, and if the profits will remain stable after you leave.

When your reports are scattered or your numbers conflict, buyers lose confidence and pull back.

You can gain the upper hand by organizing these documents before you list your practice. Proper preparation justifies a higher valuation, limits questions during due diligence, and keeps your sale on track.

Tax Returns

Buyers typically review several years of business tax returns to verify revenue, expenses, and reported income.

Tax returns establish a historical record, but they rarely tell the entire story. Buyers will compare them with profit and loss statements, payroll records, collection reports, and other financial documents.

Differences may result from accounting methods, timing, expense classifications, or owner-related costs. These discrepancies are not always concerning, but you should be prepared to explain them clearly.

Unexplained differences can make buyers question the reliability of the remaining financial information.

Profit and Loss Statements

The profit and loss statement shows how much revenue the practice generates, where the money is spent, and how much profit remains.

Buyers will closely review major expenses such as:

- Staff compensation

- Dental supplies

- Laboratory fees

- Rent

- Marketing

- Insurance

- Professional fees

- Technology

- Owner-related expenses

Use consistent accounting categories from year to year. If an expense changes significantly, document the reason.

For example, increased payroll could indicate poor cost control, or it could reflect the addition of an associate who expanded production. The buyer needs enough context to understand which explanation applies.

Balance Sheets

A balance sheet shows what the practice owns, what it owes, and how its financial position has changed.

Buyers may review loans, credit lines, accrued expenses, equipment financing, and other liabilities that could affect the transaction.

They will also want to confirm which assets are included in the sale.

Make sure the balance sheet is consistent with equipment lists, loan statements, leases, and the proposed purchase terms. Unclear ownership of equipment or other assets can create unnecessary delays late in the process.

Production and Collection Reports

Production measures the value of services performed. Collections show how much money the practice actually received.

Buyers compare the two to evaluate collection efficiency, insurance adjustments, write-offs, and the reliability of reported revenue.

A large difference between production and collections may reflect contractual adjustments, slow insurance payments, weak collection systems, or inaccurate reporting.

The numbers do not need to look perfect. They do need to be accurate and explainable.

Provider Production Reports

Buyers need to know who produces the revenue.

Reports should separate production and collections by the owner, associates, hygienists, and other providers. This helps buyers evaluate:

- How much production depends on the selling dentist

- Whether associate revenue is stable

- How productive the hygiene department is

- Whether the practice can maintain capacity after closing

A practice collecting $2 million with most production tied to one owner may present more transition risk than a practice with revenue distributed across several providers.

That difference can affect valuation, deal structure, and how long the seller may be expected to remain after closing.

Accounts Receivable Aging

An accounts receivable aging report shows what patients and insurance companies owe the practice and how long the balances have been outstanding.

Buyers will review how much AR is current and how much is more than 30, 60, or 90 days old. Older balances are generally harder to collect and may indicate weaknesses in billing or follow-up procedures.

The purchase agreement must also address whether AR is included in the sale and who will collect outstanding balances after closing.

Cleaning up aged receivables before listing the practice can improve cash flow and remove a potential negotiating issue.

Hygiene and Patient Activity Reports

Buyers use hygiene and patient activity reports to judge whether current revenue is supported by recurring demand.

- Relevant information may include:

- Hygiene production

- Active patient counts

- Recall activity

- Pre-appointment rates

- New patient trends

- Cancellations and no-shows

Strong hygiene and recall systems suggest that patients return consistently and that revenue is not dependent on a small number of large cases.

Weak patient activity may cause buyers to question whether current collections can continue under new ownership.

Insurance Participation and Fee Schedules

Prepare a list of participating insurance plans, current fee schedules, and the percentage of revenue associated with each payer category.

This information helps buyers evaluate reimbursement levels, administrative requirements, profitability, and the potential effect of changing insurance participation.

Two practices with similar collections may produce different cash flow because of their payer mix and contracted fees.

Add-Back Documentation

If you plan to adjust reported earnings for personal, discretionary, or one-time expenses, prepare an add-back schedule. For each adjustment, include:

- The expense

- The amount

- The year

- The reason it should be adjusted

- Supporting documentation

Buyers are more likely to accept add-backs that are easy to verify and unlikely to continue after the sale.

Unsupported adjustments can lead to greater scrutiny and a lower earnings calculation during due diligence.

Make Sure the Numbers Tell One Story

Consistency is the foundation of financial preparation. Tax returns, P&Ls, production reports, collection reports, payroll records, and AR should support the same overall picture of the practice.

When reports conflict, buyers may assume the practice has weak financial controls or that important information is missing. Either conclusion can reduce confidence and create pressure on price or terms.

Root Data brings financial and operational performance into one clear view, helping practice owners identify inconsistencies, track buyer-relevant metrics, and prepare before due diligence begins.

Final Thoughts

Strong financial records do more than support a valuation. They show buyers that the practice is organized, well managed, and easier to evaluate.

Before going to market, gather the reports buyers will request, resolve inconsistencies, explain unusual trends, and document every adjustment you expect them to accept.

The easier your financial story is to verify, the less likely the transaction is to be delayed by repeated questions, renegotiation, or loss of buyer confidence.

Preparing to sell your dental practice? Root Data helps you track the production, collections, hygiene, provider performance, and patient metrics buyers care about most, so you can enter the sale process with cleaner data and fewer surprises.

Want more insights like this?

Connect your practice management system to Root Data and get clear, actionable insights on your production, collections, and hygiene.

Explore Root Data