Dental Practice Add-Backs Explained: Which Expenses Count in a Valuation?

During valuation, some of those costs may be added back to earnings. Those adjustments are called add-backs. Handled properly, add-backs can present a more accurate picture of the practice’s earning power. Handled aggressively, they can damage credibility and give buyers a reason to question the rest of the financials.

A dental practice can actually be more profitable than it looks on paper.

This can happen if the profit and loss statement includes expenses that are personal, unusual, or unlikely to continue after the sale.

During valuation, some of those costs may be added back to earnings. Those adjustments are called add-backs.

Handled properly, add-backs can present a more accurate picture of the practice’s earning power. Handled aggressively, they can damage credibility and give buyers a reason to question the rest of the financials.

The issue is not whether an expense appears on the books.

The issue is whether a buyer will reasonably expect that expense to continue after closing.

What Is a Dental Practice Add-Back?

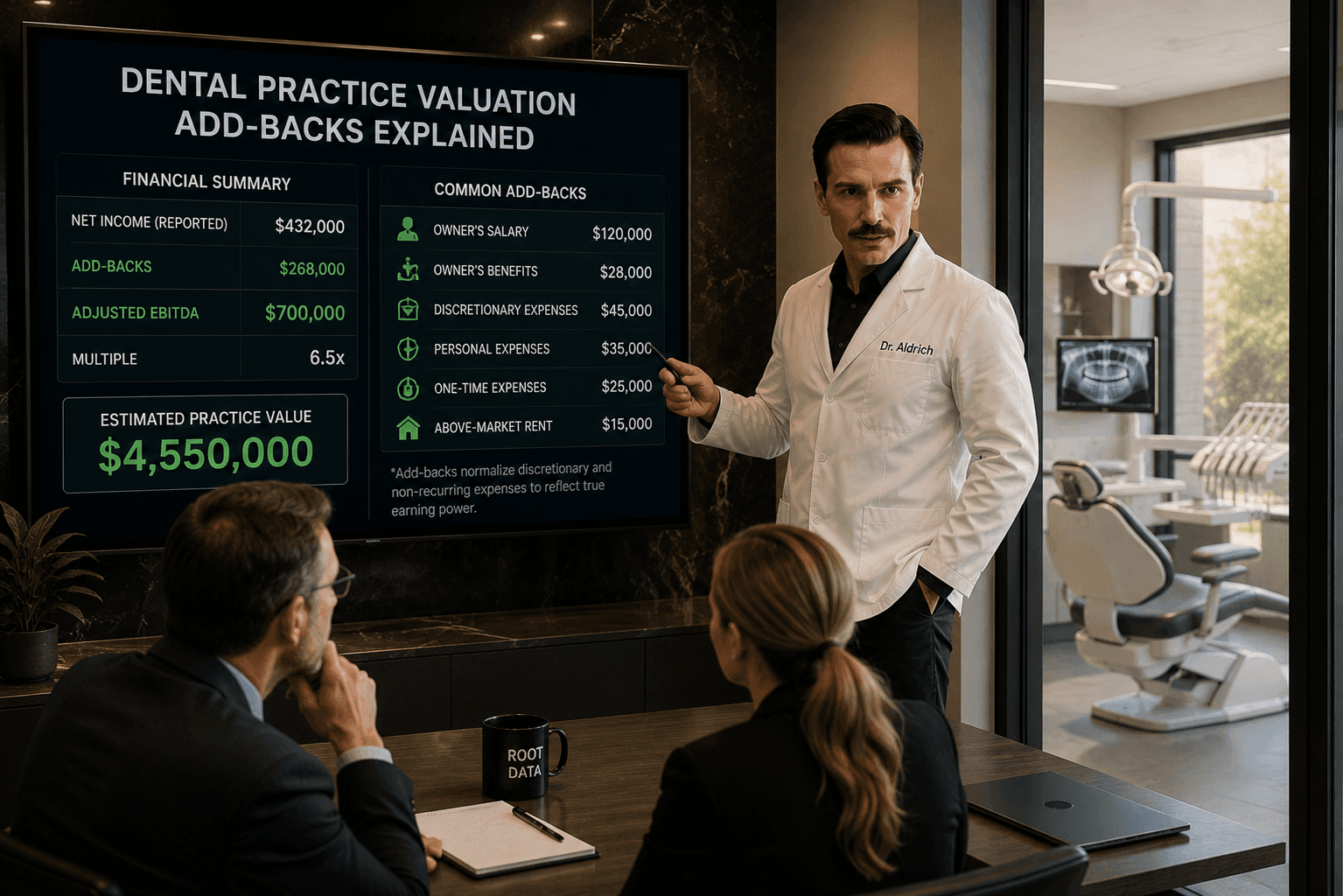

An add-back is an expense removed from the practice’s reported costs when calculating normalized earnings.

For example, suppose the practice reports $300,000 in profit. If the owner ran $20,000 of personal vehicle expenses and paid $15,000 for a one-time consulting project, those costs may not continue under new ownership.

If both adjustments are accepted, normalized earnings could increase to $335,000.

That matters because many dental practice valuations are based, at least in part, on earnings such as seller discretionary earnings or EBITDA. A higher supported earnings figure can lead to a higher valuation.

The keyword is supported.

A seller cannot simply label every undesirable expense an add-back. Buyers will expect a clear explanation and documentation.

Personal Expenses May Qualify

Some owner-specific expenses may be added back when they are not necessary for the practice to operate.

Common examples may include:

- Personal vehicle costs

- Personal travel

- Family members paid above-market rates

- Personal meals or entertainment

- Life insurance for the owner

- Personal phone or technology expenses

- Retirement contributions made for the owner

These expenses do not automatically qualify.

The seller should be able to show that they are personal, discretionary, and unlikely to continue under the buyer’s ownership.

For example, a vehicle expense may qualify if the car is primarily used by the owner for personal purposes. It may not qualify if the vehicle is regularly used for legitimate business purposes.

Buyers will look past the label and evaluate how the expense was actually used.

One-Time Expenses Can Be Added Back

A non-recurring expense may also qualify if it was unusual and is not expected to happen again.

Examples might include:

- A one-time legal dispute

- Temporary consulting fees

- An isolated repair after water or storm damage

- A special recruiting expense

- A one-time software conversion

- Extraordinary accounting or compliance costs

The strongest add-backs are easy to explain and clearly tied to a specific event.

If the same “one-time” expense appears every year, buyers may treat it as part of normal operations.

That is where sellers often lose credibility. An expense is not non-recurring simply because the owner does not want it included in earnings.

Owner Compensation Requires Careful Treatment

Owner compensation is one of the most important and most misunderstood adjustments.

In an SDE-based valuation, owner salary, benefits, and certain discretionary expenses may be added back because SDE is intended to show the economic benefit available to one owner-operator.

In an EBITDA-based valuation, the treatment may be different. The buyer may normalize the owner’s compensation to the market cost of replacing the seller with another dentist.

That means the full amount is not always added back.

If the owner pays themselves $350,000 but a replacement dentist would cost $250,000, the potential adjustment may be closer to the $100,000 difference, not the entire salary.

The correct treatment depends on the buyer type, valuation method, and whether the seller’s clinical production must be replaced.

This is one reason sellers should review add-backs with a dental-specific CPA or valuation advisor before presenting them to buyers.

Which Expenses Usually Do Not Count?

Normal operating costs generally do not qualify as add-backs simply because they reduce profit.

Examples include:

- Staff wages

- Routine marketing

- Dental supplies

- Lab fees

- Rent

- Insurance

- Software subscriptions

- Regular equipment maintenance

- Ongoing professional fees

- Ordinary continuing education

These expenses are part of operating the business.

A seller may believe a buyer could reduce some of them, but potential future savings are not the same as current add-backs.

For example, a buyer may think they can negotiate better supply pricing. That is a possible improvement after closing, not proof that current supply costs should be removed from normalized earnings.

Add-backs should reflect expenses that are genuinely personal, unusual, or unnecessary under normal ownership.

Documentation Makes the Difference

A valid add-back with weak documentation may still be rejected. Buyers will want to see where the expense appears in the financial statements, why it should be adjusted, and whether the amount can be verified.

Helpful documentation may include:

- General ledger detail

- Invoices

- Payroll records

- Insurance statements

- Vehicle records

- Contracts

- Legal bills

- Written explanations from the CPA

A clean add-back schedule should identify the expense, amount, year, reason for the adjustment, and supporting documentation.

The easier the adjustment is to verify, the less likely it is to become a point of friction during due diligence.

Aggressive Add-Backs Can Lower Buyer Confidence

Sellers sometimes try to improve valuation by stretching the definition of an add-back.

That usually backfires.

If a buyer sees questionable adjustments, they may start scrutinizing every other number more closely. What began as a disagreement over a single expense can lead to broader doubt about the seller’s financial reporting.

Aggressive add-backs can also lead to a second negotiation after the letter of intent. The buyer may reduce the purchase price once diligence shows that normalized earnings are lower than originally presented.

A conservative, well-supported earnings calculation is usually more persuasive than a larger number built on weak assumptions.

How to Prepare Your Add-Backs Before Valuation

Start by reviewing several years of profit and loss statements line by line.

Separate expenses into three categories:

- Normal operating expenses

- Personal or discretionary owner expenses

- One-time or non-recurring costs

Then gather support for every proposed adjustment. Do not wait until a buyer asks. Preparing the schedule in advance gives your CPA, broker, or valuation advisor time to challenge weak add-backs and strengthen valid ones.

Root Data can also help by giving practice owners a clearer view of expenses, profitability, and financial trends before the practice goes to market. When the underlying data is organized, it becomes much easier to identify legitimate adjustments and explain them with confidence.

### Final Thoughts

Add-backs can materially affect a dental practice valuation, but only when they reflect real economic differences between the seller’s ownership and the buyer’s future operations.

Personal expenses, one-time costs, and certain owner compensation adjustments may qualify. Routine operating expenses usually do not. The strongest approach is simple: be reasonable, document every adjustment, and assume the buyer will verify the details.

A buyer is more likely to accept normalized earnings when the numbers are clear, consistent, and easy to defend. That can support a stronger valuation and reduce the risk of price reductions later in the sale process.

Interested in selling your dental practice? Start by plugging in Root Data to get a clear idea of what is and isn't working.

The first month is free. Once that's all set up, send us an email at hello@rootdata.io.

Want more insights like this?

Connect your practice management system to Root Data and get clear, actionable insights on your production, collections, and hygiene.

Explore Root Data